Understanding the Landscape of Alternative Investments

For many, investing often means buying stocks and bonds. These traditional assets have long been the main tools for financial growth. But in today’s changing markets, focusing only on these might limit your portfolio’s power. We are seeing increasing interest in a different group of assets—alternative investments.

These special options go beyond the usual stocks, bonds, and cash. They offer new ways to spread your risk, aim for higher profits, and even protect against rising prices. As we face uncertain economic times, learning about alternatives is more important than ever.

In this comprehensive guide, we will explore alternative investments. We will explore their unique traits, ranging from private companies to physical assets such as real estate and precious metals. We will discuss their benefits for your money, examine the risks, and show how everyday investors can get into these opportunities today. For those interested in physical assets, checking out helpful places like Summit Metals can be a good start.

Alternative investments encompass a vast array of assets and strategies that fall outside the conventional categories of publicly traded stocks, bonds, and cash. Historically, these opportunities were the exclusive domain of institutional investors, such as pension funds, endowments, and ultra-high-net-worth individuals. However, the landscape is evolving, with increasing accessibility for a broader range of investors.

Key players in this space include private equity firms, venture capital funds, and hedge funds. These entities deploy significant institutional capital into diverse ventures, from acquiring established private companies (private equity) and funding early-stage startups (venture capital) to employing complex trading strategies (hedge funds). The sheer scale of this market is staggering; for instance, Blackstone became the first alternative investment manager to reach an astounding $1 trillion in assets under management (AUM) in 2023. This growth highlights the increasing importance of alternatives in global finance and explains why private equity is targeting individual investors more than ever.

The appeal of alternatives often lies in their potential for low correlation with traditional markets, which can provide a buffer during downturns. They also aim for “alpha generation”—returns above what would be expected from market movements alone—and “absolute return” strategies, which seek positive returns regardless of market conditions.

Here’s a quick comparison of traditional versus alternative asset characteristics:

Feature Traditional Assets (Stocks, Bonds) Alternative Investments Liquidity High (daily trading) Low (long lock-up periods, infrequent trading) Valuation Transparent (market prices) Complex (private, expert appraisal) Regulation High (SEC, public disclosures) Lower (often less stringent, private offerings) Correlation High (move with market trends) Low (independent performance drivers) Accessibility High (retail investors) Limited (accredited, institutional, high minimums) Fees Lower (brokerage, expense ratios) Higher (management fees, performance fees, carry) Transparency High (public filings, news) Lower (private data, proprietary strategies) Holding Period Short to long Typically long (5-10+ years) How Alternatives Differ from Traditional Stocks and Bonds

The fundamental distinction between alternative investments and traditional stocks and bonds lies in their market structure and underlying characteristics. Traditional assets operate within highly regulated public markets, offering daily liquidity and transparent pricing. Their performance is often closely tied to broad economic cycles and market sentiment, leading to high correlation.

In contrast, many alternative investments reside in private markets. This means they are not publicly traded, leading to infrequent valuations and significantly lower liquidity. While this illiquidity can be a drawback, it also means these assets are less susceptible to daily market volatility, potentially offering more stable returns over the long term. Their unique drivers of value—such as operational improvements in a private company or rental income from a specific property—can provide genuine diversification, helping a portfolio “zig” when public markets “zag.”

The Performance of Private Markets vs. Cash

One of the most compelling arguments for including alternatives in a portfolio is their historical performance, particularly when compared to traditional assets like stocks and cash. The statistics speak volumes:

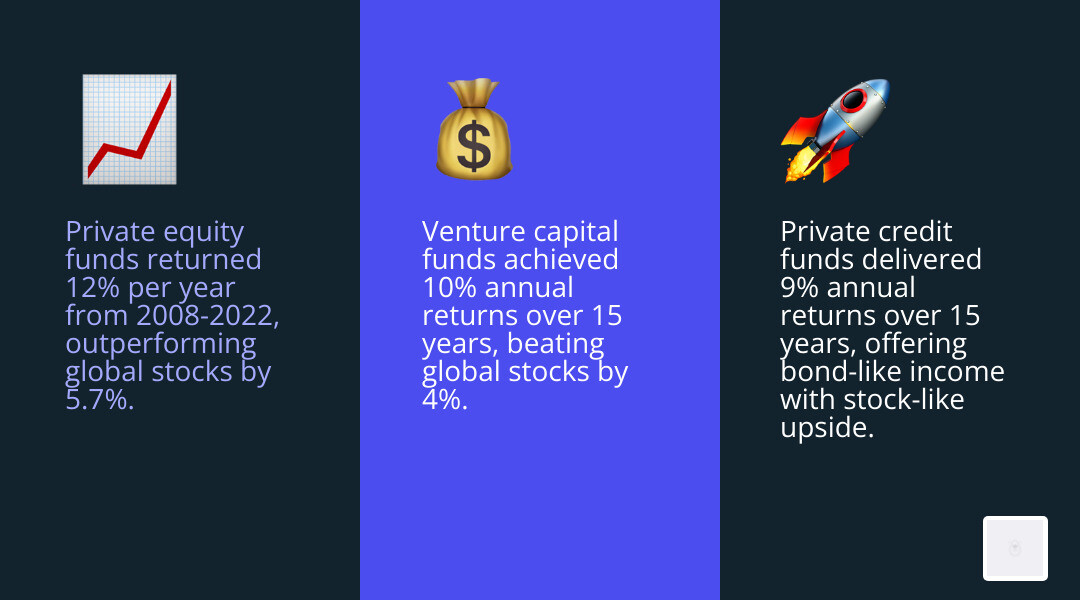

- From 2008 to 2022, private equity funds returned about 12% per year, significantly outperforming global stocks by 5.7%. This consistent outperformance underscores the potential for higher returns when investing in private companies.

- Private-credit funds, which involve direct lending to businesses, have delivered robust returns of 9% per year over the past 15 years. This asset class offers a bond-like income stream but with stock-like returns, often filling a gap left by traditional bank lending.

- Venture capital funds focused on high-growth startups returned almost 10% per year over 15 years, outperforming global stocks by approximately 4%. While inherently riskier, successful venture investments can yield substantial returns.

These figures demonstrate that private markets have historically offered attractive risk-adjusted returns, making them a powerful component for long-term portfolio growth and diversification.

Tangible Assets: The Strategic Role of Real Estate and Infrastructure

Beyond the financial intricacies of private equity and venture capital, tangible assets such as real estate and infrastructure are another cornerstone of alternative investments. These assets provide a direct link to the physical economy, offering unique benefits such as inflation protection, steady income streams, and tangible value.

Real estate investments can take many forms, from direct property ownership and real estate investment trusts (REITs) to more specialized funds focused on commercial, residential, or industrial properties. Infrastructure assets, such as toll roads, airports, and energy transmission lines, represent essential services that generate predictable cash flows, often backed by long-term contracts. These assets are beautiful during periods of inflation, as their revenues and values tend to rise with the cost of living. For those interested in exploring property as a diversified asset, understanding the nuances of Real estate alternative investments can be highly beneficial.

Moreover, real estate offers potential tax advantages, including depreciation benefits and the ability to defer capital gains through 1031 exchanges (in the U.S.), further enhancing its appeal as a long-term investment.

Infrastructure as a Stabilizing Asset Class

Infrastructure stands out as a stabilizing force within an investment portfolio. These assets are typically characterized by project finance structures, involving long-term contracts (often 20-30 years or more) with governments or large corporations. This provides a high degree of revenue predictability and stability.

Investments in renewable energy projects, for example, fall into this category, offering not only environmental benefits but also stable, inflation-linked returns. The essential nature of infrastructure services means demand is relatively inelastic, providing a strong defensive characteristic during economic downturns. For institutional investors and, increasingly, for individuals through specialized funds, infrastructure offers a compelling combination of consistent cash flow, inflation hedging, and diversification.

Barriers to Entry and the Democratization of Property

Despite the attractive characteristics of real estate and infrastructure, significant barriers to entry have traditionally limited access for individual investors. Direct investment in large-scale commercial properties or infrastructure projects often requires substantial minimum investments, typically in the millions of dollars. Furthermore, many private real estate funds are open only to accredited investors who meet specific income or net worth thresholds.

However, the investment landscape is changing. The rise of equity crowdfunding platforms and fractional ownership models is democratizing access to property investments, allowing individuals to invest smaller amounts in projects that were once out of reach. While you might not be buying a Van Gogh painting for $81 million, these new avenues make it possible to participate in real estate and other tangible assets with more manageable capital.

Precious Metals as a Strategic Alternative Investment

Precious metals, particularly gold and silver, have served as stores of value and mediums of exchange for millennia. In modern portfolios, they are often considered strategic alternative investments, offering unique benefits such as wealth preservation, inflation hedging, and savings during economic or geopolitical turmoil.

The value of gold is often influenced by its spot price, which reflects global supply and demand dynamics. Investors engage in “silver stacking” or gold accumulation to build tangible wealth. The question of “is gold a good investment” frequently arises, and its role as a hedge against fiat currency devaluation and central bank demand for physical gold often points to its enduring appeal. When governments print more money, the purchasing power of paper currency can decline, making finite assets like precious metals more attractive.

Comparing Physical Bullion Formats

When investing in physical precious metals, investors often choose between coins and bars. Each format has distinct characteristics that cater to different investment goals and preferences.

Feature Gold Coins (e.g., American Eagle, Maple Leaf) Gold Bars (e.g., 1 oz, 10 oz, kilo) Face Value Yes (often symbolic) No Fraud Protection High (government mints, security features) Moderate to High (trusted refiners, serial numbers) Legal Tender Yes (in issuing country) No Portability High (smaller denominations, easy to carry) Moderate (larger sizes can be cumbersome) Premiums over Spot Higher (collectibility, minting costs) Lower (closer to spot price, less intricate production) Liquidity High (widely recognized, easy to sell) High (widely accepted by dealers) Divisibility Good (various sizes, including fractional) Good (vmultiplesizes, including fractional) For many investors, the decision often comes down to balancing premium costs with the desire for smaller, more liquid units. Understanding “the benefits of buying fractional gold” can be crucial for those looking to build a diversified physical metals portfolio without waiting for larger, more expensive pieces.

Automating Wealth with Autoinvest Strategies

For those looking to consistently build their precious metals holdings, “autoinvest” programs offer a convenient and disciplined approach. Similar to dollar-cost averaging strategies in traditional investments, these programs allow investors to set up recurring purchases of gold, silver, or other metals.

This method helps to mitigate the impact of market timing, as investments are made regularly regardless of price fluctuations. It’s a 401 (k)- style approach to buying precious metals, fostering consistent accumulation over time. By automating purchases, investors can gradually build a substantial physical metals position, aligning with a long-term stacking strategy and reducing the emotional decision-making often associated with market volatility.

Navigating Risks, Fees, and the Path to Liquidity

While alternative investments offer compelling benefits, they also entail unique risks and considerations that require careful attention. Understanding these aspects is crucial for making informed decisions and managing expectations.

One of the most significant characteristics of many alternative assets is illiquidity risk. Unlike publicly traded stocks or bonds that can be bought and sold daily, alternatives often involve long lock-up periods, limited trading windows, or simply a lack of readily available buyers. This means your capital may be tied up for years, making it difficult to access funds quickly if needed. For instance, selling a substantial amount of 10 oz silver alternative investments might be straightforward with a reputable dealer, but offloading a stake in a private equity fund or a large piece of art can take considerable time and effort.

Management fees for alternative investments are typically higher than those for traditional funds. These often include an annual management fee (e.g., 1-2% of AUM) and a performance fee (e.g., 20% of profits above a specific hurdle rate), known as “2 and 20” in the hedge fund world. Investors must conduct thorough due diligence to understand the fee structure and its potential impact on net returns.

Other risks include counterparty risk (the risk that the other party in a transaction will default), capital calls (in private equity, where investors commit capital but only fund it when needed), and the aforementioned lock-up periods. The complexity of these structures necessitates a more profound understanding than traditional investments.

Establishing a Robust Exit Strategy

Given the illiquid nature of many alternatives, establishing a robust exit strategy from the outset is paramount. For physical precious metals, this might involve utilizing private vault storage facilities that offer integrated “sell to us” programs, ensuring a transparent and efficient path to market liquidity. Reputable dealers often provide instant liquidation options, allowing investors to sell their bullion back at competitive prices, sometimes after an asset assay to verify purity and weight. This is particularly important for investments like a precious metals IRA; understanding your options for liquidating assets within an IRA is essential for future financial planning.

For private equity or real estate funds, the exit strategy is typically dictated by the fund’s lifecycle, often involving an IPO, sale to another company, or recapitalization. Investors need to be comfortable with these extended timelines and the potential for delays.

The Impact of Fees and Expenses on Total Returns

The higher fee structures prevalent in alternative investments can significantly impact an investor’s total returns. Understanding the various components—such as expense ratios, performance fees, and carry interest (a share of profits taken by the general partners in private funds)—is critical. Additionally, storage costs for physical assets and transactional friction (brokerage fees, legal costs) can erode returns. While these fees are often justified by the specialized expertise and active management involved, investors must scrutinize them to ensure they align with the potential value added. A transparent fee structure and a clear understanding of how costs are calculated are hallmarks of a well-managed alternative investment.

Accessing the Market: From Private Credit to Liquid Alternatives

The world of alternative investments, once an exclusive club, is becoming more accessible. While direct investment in large-scale private equity funds or complex hedge fund strategies remains largely for institutional and accredited investors, new avenues and products are emerging to bridge this gap.

Private credit has gained significant traction as an alternative asset class. This involves direct lending to companies, often those overlooked by traditional banks, offering attractive yields and diversification benefits. It includes strategies such as direct lending, distressed-debt investing (investing in the debt of financially troubled companies), and mezzanine financing (a hybrid of debt and equity). For insights into how this can offer lower-risk private credit and competitive returns, it’s worth exploring how these funds operate.

The Rise of Liquid Alternative Investments

Perhaps the most significant development in democratizing alternative strategies is the rise of liquid alternative investments. These are mutual funds or exchange-traded funds (ETFs) that employ alternative methods—such as short selling derivatives or leverage—but offer daily liquidity, lower minimums, and regulated structures. They aim to replicate the benefits of hedge funds or private market exposure in a more accessible format.

The growth of liquid alternatives has been substantial, with assets under management (AUM) growing from $124 billion in 2010 to $310 billion in 2014. Firms like AQR Capital Management have seen significant growth, driven in part by the popularity of liquid alternative mutual funds. These products allow individual investors to gain exposure to sophisticated strategies that were once out of reach, potentially enhancing diversification and risk-adjusted returns without the illiquidity constraints of traditional alternatives.

Sophisticated Strategies: Derivatives and Hedging

At the core of many alternative strategies, particularly hedge funds and liquid alternatives, are sophisticated financial instruments such as derivatives. Derivatives are financial contracts whose value is derived from an underlying asset, such as stocks, bonds, commodities, or currencies. They are powerful tools used for various purposes:

- Hedging: Using derivatives to offset or reduce the risk of an existing investment. For example, an investor holding a stock might buy a put option to protect against a price drop.

- Leverage: Gaining exposure to a significant underlying asset value with a relatively small amount of capital.

- Speculation: Betting on the future price movements of an asset.

Common types of derivatives include:

- Call options: Give the holder the right, but not the obligation, to buy an asset at a specified price (strike price) before a specific date.

- Put options: Give the holder the right, but not the obligation, to sell an asset at a specified price (strike price) before a specific date.

- Futures contracts: Standardized agreements to buy or sell an asset at a predetermined price on a specific future date.

- Swaps: Agreements to exchange cash flows or other financial instruments over a period.

The “notional value” of a derivative refers to the total value of the underlying asset controlled by the contract. Derivatives enable efficient capital deployment and precise risk management, enabling strategies such as arbitrage (profiting from price differences across markets) and short selling (profiting from a decline in an asset’s price).

Frequently Asked Questions about Alternative Investments

As alternative investments become more mainstream, many questions arise regarding their suitability, risks, and practical implications. Here, we address some of the most common inquiries.

Who is eligible to invest in private alternative assets?

Traditionally, direct investment in private alternative assets, such as private funds and hedge funds, has been restricted to accredited investors. In the U.S., this typically means individuals with a net worth exceeding $1 million (excluding their primary residence) or an annual income of $200,000 ($300,000 for married couples) for the past two years, with an expectation of the same in the current year. These requirements are in place to ensure that investors have the financial sophistication and capacity to absorb the higher risks and illiquidity associated with these investments.

However, as discussed, the landscape is shifting. Retail investors are gaining access through vehicles like liquid alternatives (mutual funds and ETFs) and interval funds, which pool capital to invest in less liquid assets while offering periodic redemption opportunities. Equity crowdfunding platforms also allow non-accredited investors to participate in early-stage private companies, albeit with specific investment limits.

What are the primary drawbacks of including alternatives in a portfolio?

While the benefits of alternative investments are compelling, it’s crucial to acknowledge their drawbacks:

- High Minimum Investments: Many alternatives, especially private funds, require substantial capital commitments, often $100,000 or more.

- Complexity: The strategies and structures can be intricate, requiring a high degree of financial literacy to understand.

- Lack of Transparency: Private markets often have less regulatory oversight and disclosure compared to public markets, making it harder to evaluate underlying assets and strategies.

- Limited Historical Data: Because of their private nature, comprehensive historical performance data can be scarce, making it difficult to assess long-term risk and return.

- Extended Holding Periods and Illiquidity: As mentioned, capital can be locked up for many years, limiting access to funds.

- Higher Fees: The specialized management and operational complexities often translate into higher fees, which can erode returns.

These factors underscore the need for thorough due diligence and a clear understanding of your personal financial situation before committing to alternative investments.

How do collectibles like art and wine compare to financial alternatives?

Collectibles, such as fine art, rare wines, stamps, or even unique memorabilia, represent a distinct category of tangible alternative investments. Unlike financial alternatives, which often involve complex strategies, collectibles derive their value from rarity, historical significance, artistic merit, and collector demand

Their valuation is often subjective and can be highly volatile, dependent on trends and the whims of the market. A famous study by William Baumol in 1986 found that the average real annual return on art investments over 410 years was a modest 0.55%. While some individual pieces can achieve astronomical prices—like the Van Gogh example mentioned earlier, or even a lock of Mick Jagger’s hair auctioned as a novelty item—the overall market for collectibles often underperforms financial assets.

Key considerations for collectibles include:

- Storage Requirements: Proper storage (climate control, security) is essential and can be costly.

- Insurance: Protecting valuable items requires specialized insurance.

- Authenticity and Provenance: Verifying the origin and legitimacy is crucial to value.

- Lack of Income: Collectibles typically do not generate income or dividends.

- Passion Investments: Often, the primary driver for investing in collectibles is personal enjoyment or passion, rather than purely financial returns.

While they can offer diversification and a hedge against inflation for some, their illiquidity, high transaction costs, and subjective valuation make them a niche choice, often best suited for those with a deep understanding and passion for the specific asset class.

Conclusion

The investment landscape is continually evolving, and the role of alternative investments is more prominent than ever. From the strategic growth opportunities in private equity and venture capital to the stabilizing influence of real estate and infrastructure, and the enduring appeal of precious metals, these assets offer powerful tools for portfolio diversification and enhanced returns.

While alternative investments come with their own set of complexities—including illiquidity, higher fees, and accessibility barriers—the expanding market for liquid alternatives and fractional ownership models is making them increasingly available to a broader investor base.

For those seeking to future-proof their wealth and build financial resilience, a thoughtful allocation to alternatives, combined with thorough due diligence and a long-term vision, can be a transformative step. By understanding the unique characteristics, benefits, and risks of these diverse assets, investors can strategically position their portfolios to thrive in an ever-changing economic environment.

{kind=link}