Key Takeaways

- Homeowners are frequently challenged by delayed processing and underpayment during insurance claims.

- Being familiar with policy exclusions and the 80 percent rule can help avoid setbacks.

- Maintaining thorough documentation and regularly reviewing your policy reduces the risk of claim complications.

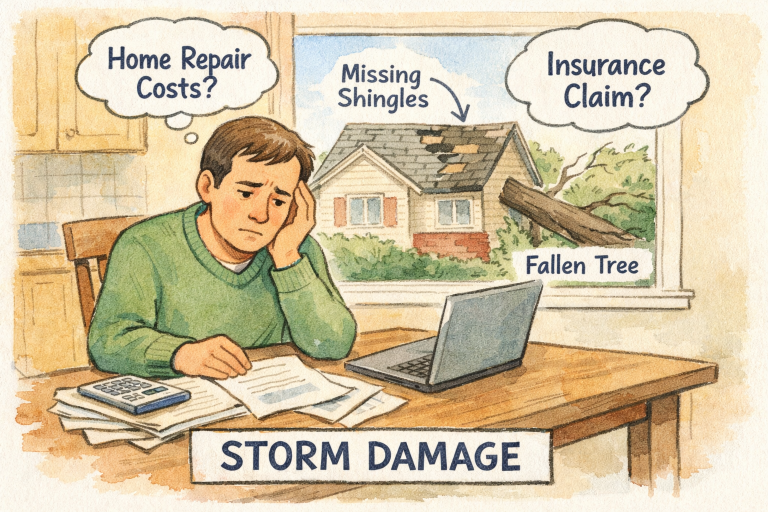

Home insurance claims are an inevitable part of homeownership, especially when unexpected events cause damage or loss. The process may seem straightforward at first, but many homeowners encounter pitfalls that can delay settlements or reduce payouts. Knowing how the insurance process works and what obstacles you might face can help you secure the compensation you deserve. For homeowners in Florida, understanding local regulations and the claims process is especially important. If you need to learn more about the specifics of filing insurance claims in Tampa, there are resources available to guide you through the unique challenges present in the region.

Many homeowners meet challenges such as extended processing times, unclear policy language, or difficulty obtaining full payment for damages. Navigating these issues can be complicated, and a lack of familiarity with your policy can leave you overwhelmed. When disasters strike, being prepared and well-informed becomes even more crucial for a smooth claims process.

Understanding the nuances of insurance claims means recognizing how exclusions, claim documentation, and coverage limits work in practice. While most policies cover a broad range of incidents, there are important limitations to note. Consulting experts and regularly reviewing your policy help avoid unpleasant surprises when a claim is necessary.

Another area of concern for policyholders is the range of claim types, including the distinction between coverage for structural damage versus contents. This is especially relevant when dealing with complex property claims that may involve multiple areas of a home, different causes, or various forms of evidence.

Delays in Claim Processing

Extended wait times are one of the most common frustrations for homeowners filing insurance claims. According to J.D. Power data, average claim settlement times have increased to over 44 days. Several factors can prolong the process, including the rise in catastrophic weather events and the resulting demand on adjusters. Insurers may also require additional documentation or repeatedly request more details, further delaying resolutions. These hold-ups can be stressful, particularly when urgent repairs are needed for the property.

Underpayment of Claims

Beyond delays, homeowners sometimes receive offer amounts from insurers that fall short of what is needed for full repairs or replacements. This issue can occur when insurers use software estimates that may not reflect localized labor or material costs, or when they apply depreciation formulas to certain types of property. Another tactic involves categorizing damages to reduce payout obligations. Securing independent repair estimates and questioning discrepancies can help address concerns about underpayment.

Policy Exclusions and Coverage Gaps

Policy exclusions are another major area where homeowners face setbacks. Standard home insurance often does not cover events like flooding, earthquakes, or sewer backups. This leaves homeowners exposed to high out-of-pocket costs unless they have purchased separate riders or special coverage. Understanding your policy and regularly confirming what is and isn’t included helps prevent expensive surprises after incidents occur. Government programs like FEMA’s National Flood Insurance Program exist to fill some of these coverage gaps, but require advanced enrollment.

The 80% Rule in Home Insurance

The 80 percent rule is a lesser-known policy condition with potentially major consequences. It requires homeowners to insure their property for at least 80 percent of its current replacement cost. Failure to do so may result in lower payout percentages when you file a claim. Insurers use this rule to ensure policyholders have appropriate coverage relative to the value of their homes, thereby minimizing their own risk of underinsurance. Policyholders should periodically review and update their coverage amounts, especially after significant renovations or increases in property value.

Importance of Documentation and Mitigation

Thorough documentation can make or break a successful insurance claim. Keeping detailed records, including recent photos, receipts for big-ticket items, and records of renovations, supports your case in the event of a dispute. After an incident, documenting damages promptly and taking reasonable steps to prevent further harm, such as placing temporary tarps over roofs or removing standing water, is critical. Insurance companies may fail to process your claim or reduce payment if they determine the homeowner did not act to minimize the loss.

Rising Premiums and Policy Non-Renewals

Many homeowners have noticed changes in renewal rates or outright non-renewals as insurers reassess their risk profiles, especially in regions prone to hurricanes, wildfires, or flooding. Premium increases and policy restrictions are becoming common. Policyholders should routinely review renewal offers for changes in coverage terms. Exploring policy options with other insurers or seeking risk-reducing adjustments, such as stormproofing windows, can help maintain affordable, continuous insurance coverage.

Practical Steps for Homeowners

- Review Your Policy Regularly: Set aside time at least once a year to read your policy documents and understand coverage limits and exclusions.

- Maintain a Home Inventory: Keeping an updated list or photographic record of your home’s contents helps substantiate claims.

- Act Quickly After a Loss: Take prompt steps to mitigate damage and begin documenting the incident immediately.

- Seek Professional Help If Needed: If your claim faces significant hurdles, consider consulting a public adjuster or a legal professional with experience handling complex claims.

With rising costs, increasing claims, and more complex climate risks, homeowners must be vigilant about documenting their property, understanding their policy, and taking proactive steps to protect themselves from coverage disruptions.

Conclusion

Navigating home insurance demands awareness, preparation, and proactive decisions. Challenges like delayed claims, underpayments, coverage gaps, and changing insurer rules can impact recovery. Understanding policies, maintaining documentation, and knowing rules like the 80% requirement are vital to protect your investment. Being prepared—by reviewing coverage, taking preventive actions, and consulting experts—helps homeowners manage claims effectively and secure protection in a complex insurance landscape.

{kind=link}